This Blog provides you UpToDate information on life & General insurance dealing mostly with LIC's New Plan Circulars, MillionDollarRoundTable tips on marketing,Financial analysis and INCOME TAX.

DEAR AGENT FRIENDS

DEAR AGENT FRIENDS,

PL DONT ENTER EMAIL IDS OF UR CLIENTS IN LIC RCT DETAILS.

LIC IS STEALING THOSE IDS AND GIVING THEM TO LIC DIRECT MARKETING.

FEW DAYS BACK I HV ENTERED MY EMAIL ID TO MY OWN RCT-- I HV STARTED

GETTING REGULAR EMAILS FOR BUYING NEW POLICIES FROM DIRECT MARKETING

--WE HV TO TAKE THIS MATTER WITH LIC MANAGEMENT.

ASK THEM TO STOP CHEATING THE AGENTS

some of our friends writen this letter but it is true

Government propose to amend the Insurance Act 1938

You all are aware that the Government and IRDA propose to amend the Insurance Act 1938 in the coming session of Parliament. These proposed amendments in the act will:

1. Stop payment of balance commission and gratuity to the widow of an agent, means the hereditary commission goes,

2. Powers of the Parliament to decide the rates at which commission to a life insurance agent of LIC as well as that of a private insurer have to be paid, will be transferred to IRDA. Means the rates of commission will be decided by IRDA.

3. Delete the provision of prohibition of stopping of payment of commission to insurance agents.

These amendments will dismantle the agency structure in India prepared after years of hard work and after spending hundreds of crores.

This will cause lakhs of crore loss to the Government in the form of premium not received which is being utilized for long term investment in the infrastructure development of the country. The story of mutual fund, PPF and General insurance is before us where in business has been badly reduced due to neglect of insurance advisors/agents.

Please recall the recent draconian suggestions made by Devendra Swaroop committee to stop payment of commission to us.

In the light of the above we have decided to launch nation wide agitation against these proposed amendments in the Insurance Act.

vinay mohanty

rajnathsnigh and others assure they will do best

vinay mohanty

agent can take3 agencis life/general/Health

NOW ANY insurance AGENT CAN TAKE 1.ONE AGENCY OF GENERAL INSURANCE. 2.one AGENCY OF A HEALTH INSURANCE .and 3.one Lifeinsurance agency LETEST INFORMATION.

vinay mohanty

vinay mohanty

IRDA new chief TSVijayan

21 February 2013

Vijayan, 60, takes over from J Hari Narayan who ended a five-year tenure on Wednesday.

The IRDA head is appointed for a term of five years or till the age of 65 years.

An IRDA statement said Vijayan has taken charge as its chairman today.It is a comeback for Vijayan who was demoted to managing director of LIC following charges of financial irregularities. He had also taken voluntary retirement in November 2012.

Vijayan, who was battling corruption allegations with regard to investment decisions made by LIC during his tenure, however, got a clean chit from the Central Bureau of Investigation (CBI) and the finance ministry.

http://www.domain-b.com/finance/insurance/irda/20130221_vijayan.html

vinay mohanty

Insurer’s Managed Funds to Touch Rs30 lakh crare Mark in 5 yrs: IRDA Chairman

The size of funds managed by insurers in the country is expected to reach whopping level of Rs 30 lakh crores in next five years, a jump of 70% from current level, outgoing Insurance Regulatory and Development Authority (IRDA) chairman J. Hari Narayan said.

He said that when the insurance industry was opened up in 2000, the total controlled fund was about Rs 1 lakh crores. It was Rs 8 lakh crores in 2008 and it is Rs 18 lakh crores now.

He also said that he is in favour of government’s view of hiking Foreign Direct Investment (FDI) limit in insurance sector to 49% from current 26%. This would lead to a substantial flow of funds in capital intensive sector. It is estimated that insurance sector will require at least Rs 30,000 crores in next five years to double its size.

vinay mohanty

The total investment corpus of LIC has touched Rs 14.8 lakh crores

The total investment corpus of Life Insurance Corporation of India (LIC) has touched Rs 14.8 lakh crores (provisional) as of 31 December 2013 as against Rs 13.49 lakh crores at the end of December 2012, registering a growth of 10% in first nine months of this fiscal.

Investment in government securities accounted for a major chunk in LIC’s investments with investments worth Rs 7.27 lakh crores. Housing and infrastructure investments stood at Rs 1.91 lakh crores. And the rest included investments in the corporate sector and project loans.

Central government securities contributed Rs 4.77 lakh crores, followed by state government and other government guaranteed marketable securities.

Among housing and infrastructure investments, LIC has maximum amount of investments in the power sector, contributing Rs 94,294 crores.

This was followed by housing with Rs 41,900 crores. Other areas in infrastructure included irrigation, road, bridges, port and telecom.

LIC is expecting to invest a total of Rs 2.4 lakh crores in bonds, equities and government securities in the current financial year.

In terms of performance of different distribution channels, out of the first premium income, Rs 1,486 crores came from the chief life insurance advisor. Bancassurance and alternative channels contributed Rs 870.63 crores and direct marketing contributed Rs 218 crores.

vinay mohanty

Does FDI 49% benefit the common man?

Does this benefit the common man?

This change does not benefit the common man, as he is the target for all insurance companies, whether Indian or foreign, who try to extract maximum business from the gullible public, who are carried away by the sweet talk and tall promises made by the insurance salesmen. In fact they are concerned more about their own commission rather than the welfare of the insured. Insurance business is one where there is rampant mis-selling and the insurance companies go scot free because of a number of conditions included in the policy in small print, but never communicated in advance.

Our country has a low insurance density and every company selling the insurance feels that there is abundant scope to expand its operations and hence this proposal to increase FDI in insurance has been received with great applause by the industry. Only time alone will tell whether this irrational exuberance is justified considering the fact that there is political opposition to this move and this change requires approval of the Parliament.

If and when this proposal becomes a law there is bound to be a great demand from foreign companies to enter our country because of the abundant opportunity provided by the large population and the growing per capita income of our people. During the last twelve years, if over 40 foreign companies have entered our country as joint venture partners, with the increased FDI cap, we may expect another 100 companies to come within the next twelve years. Unfortunately, some of our people are carried away by the foreign names and brands, and that there is a perception among our people that foreign companies are better than the home-grown companies. But the fact is that foreign companies are as bad as or as good as local companies, and insurance business, whether run by Indians or by foreigners has the same objective, as in all business, of maximizing returns to the owners even at the cost of the insured.

How to protect “aam aadmi” from exploitation by the insurance companies?

It is abundantly clear that mere hiking the FDI cap to 49% does not in any way benefit the common man, unless it is accompanied by stringent regulations to protect the “aam aadmi” from exploitation.

Once the Insurance Amendment Bill is passed

Once the Insurance Amendment Bill is passed, it is expected to remove lot of operational hurdles and is expected to align the provisions of the 1938 Act in line with the current industry requirements, CL Baradhwaj says | ||

STUDY RIGHT

There is one straight road to success in selling. It's paved with knowledge. Competency never lacks opportunity."

STUDY RIGHT

We believe you create a future, characterized by high performance and fulfillment, by making a responsible commitment to think right, work right, sell right, study right, and live right.

Here are ten strategies for forming the habit of studying right.

. Be a student of selling. In a world of change, you are never completely educated. You must keep educating yourself to cope with change. The more you learn about your job, the less fear there is. Fear is born out of ignorance.

. Prepare well. Spectacular performances are always preceded by spectacular preparation. Cultivate the will to prepare.

. Develop a mentor. Self-talk shapes your selling life. Take charge of your thoughts. Monitor what you are telling yourself about your situation and about your potential in selling.

. Watch your self-talk. Learn as much as possible about your prospects -- their reputations and capacities, who they are buying from now and what they are receiving for their dollars. Decide to be a shrewd observer.

. Stay brilliant on the basics. Rely on these fundamentals: Build credibility, be well mannered, simplify your recommendations, speak prospect's language, speak as one having authority, sell at your buyer's pace, avoid exaggeration and dogmatic statements, use repetition, make it the prospect's idea, summarize strategically, and close with confidence.

. Achieve competency levels. Become known for what you know. This is the high payoff. Now, your reputation precedes you.

. Write effectively. Simplicity is the formula for successful communication.

. Develop the slight edge. This principle has to do with what a slight improvement in one skill can do to your performance over a period of time.

. Out-distance competition. To out-distance your competition you must learn more and better ways to out-serve them. You then become your own best recommendation.

. Build your Research and Development Department. Develop a library of sales support material to stay current on your products and keep you sharp on new selling techniques. Subscribe to sales publications, and utilize the resources available on the Internet.

"GO ALL OUT - NO IN BETWEEN IN 2013!"

Good luck and good selling,

Jack and Garry Kinder

New insurance FDI plan to end oppn

Written by Bimabazaar- Adminstrator

Monday, 10 December 2012 11:55

Having secured Parliament’s approval for foreign direct investment (FDI) in multi-brand retail, the government is considering tweaking the planned amendments to insurance laws to win over opposition parties’ support for reforms in this key sector.

As per a fresh plan prepared by the finance ministry, the government plans to propose keeping the FDI cap in the insurance sector at 26% and allowing another 23% as foreign institutional investment (FII). Key members of the standing committee on finance from the Opposition have indicated their willingness to consider this proposal, which could also speed up listing of insurance companies on the exchanges.

This compromise formula is being prepared as the UPA government is bound to face stiff opposition to an earlier plan to raise the FDI cap insurance to 49% from 26%. The standing committee on finance had opposed any increase in FDI limits in the insurance sector.

Sources said the new proposal has the approval of finance minister P Chidambaram, and the government is trying to securing opposition parties' concurrence on it.

Bhartruhari Mahtab, Biju Janata Dal MP and a member of the standing committee on finance, told FE: “We have given our report to maintain the FDI cap at 26% in the insurance sector, and not raise it to 49%.” When asked about the new proposal being prepared by the government, he said: “Let the suggestion come to us (the standing committee), then we will take a call. Personally, I think it will be premature to react right now."

FE could not reach senior BJP leader Yashwant Sinha – chairman of the committee – recently. But in an interview to FE last month, Sinha had said that the government could bring the new proposal – 26% FDI and 23% FII and overseas corporate bodies – to the committee for its views.

Mahtab said that before bringing in the 26% FDI plus 23% FII proposal, the government will have to withdraw the changes being proposed to the existing Bill and the new proposals will have to be routed through Parliament afresh.

Finance ministry sources said permission to portfolio investment in the insurance sector could be pushed through executive orders. None of the insurance companies are listed on stock exchanges in India now. The Securities and Exchange Board of India recently unveiled norms for initial public offerings by insurance companies.

“The government can come to the standing committee with this; it hasn’t so far. That’s when we will decide,” Sinha had said.

http://www.financialexpress.com/news/new-insurance-fdi-plan-to-end-oppn/1042785/2

vinay mohanty

Set up a system to make it easy for people to give you referrals.

Set up a system to make it easy

for people to give you referrals.

Would you like to have your clients, friends and family tell all of their co-workers, friends, family and everyone else they know about you?

Then let's start with some basic truths!

The reason most agents and advisors have trouble getting referrals is that people don't generally talk about salespeople! What is there to talk about? Except maybe negatives?

However, they do talk about people who have made a real, positive difference in their lives! They tell people about the accountant who saved them thousand of dollar on income taxes! They talk about the doctor who helped them to finally quit smoking! Or, the attorney who helped them to avoid a costly lawsuit!

The talk about people who have actually helped them solve a problem(s). They talk about the people who have gone beyond what was expected. The talk about people they like, trust and respect.

So if you want people to talk about you, and tell all of their co-workers, friends, family and everyone else they know about you, then make yourself referable!

Making yourself referable means creating value from the customer's perspective. It sounds obvious, but your products and services have value directly in proportion to how well the customer perceives that your product/service solves a serious problem they have, or creates an opportunity for them. For example, does it allow them to have more income to do the things they want to do in retirement, or does it help the client enhance their eligibility for college financial aid because of some special feature.

You can't create your value proposition and sell value unless you identify critical information from the customer. The best way to create value is to help the prospect to identify a problem or opportunity for themselves. by asking Questions during a thorough fact-find!

Remember, 'Good enough' never is! Even excellent service is probably not enough to get people to talk about you, to attract the clients you really want. Only extraordinary service will draw the world to you!

Give away valuable extras: free reports, newsletters and seminars.

Teach a course and offer free educational workshops.

Help clients and prospects to identify and solve their main problems. Not just the problems that you can make money on.

Provide service before your clients ask.

Conduct regular annual reviews, client workshops, client surveys and client appreciation events. Don't wait for your clients to call you with their questions or a problem.

Learn from every mistake. Your customers, especially the unhappy ones, are your best Research & Development team! Call them, ask questions and learn from them.

This extreme service attitude will draw the world to your door!

vinay mohanty

If bimabill 2012 passe in lokosabha

10/2/2013 The BIMA Bill 2012

passed by Lok Sabha recently would come into force after its approval by the

Rajya Sabha and assent by the President of India. The new law will have far

reaching impacts, especially in areas where we as professionals are most

concerned. Significant proposed amendments will be deliberated upon in the

emergent meeting.

VIEWS:-1.FDI Partners in

the Indian Insurance Companies from 26% to 49%

2.Existing Provision on Insurance Act 1938

Sec40,40A,41,44,45(Commission or otherwise for procuring business, Limitation

of expenditure on Commission, Prohibition of rebates, Prohibition of cessation

of payment of commission, Interest of policy

holder.

3.Amendments proposed to be made

by IRDA.(Penalty,Commissione ,Few Sec omitted.

4.Expectations of LIAFI (Hereditary commissione our right,no

changes agent commissione,Need to be preserved as it is &others benefit.

JAGO

-- INSURANCE AGENT

Protest INSURANCE AMENDMENT BILL -2008

"AN

OBSTACLE MAY BE EITHER A STEPPING STONE or

A

STUMBLING BLOCK "

vinay mohanty

reliance-life-ulip-mis-selling-justice-served

http://www.moneylife.in/article/reliance-life-ulip-mis-selling-justice-served/31172.html

vinay mohanty

vinay mohanty

Investors lost Rs.1.5 trillion due to insurance mis-selling says Mr chidambarm FM article from live mint

New Delhi: Finance minister P. Chidambaram couldn’t have been more spot-on when he spoke this week about what’s hurting the insurance industry’s growth in India.

“In my view, the reason why insurance is stumbling in India is because of mis-selling of products and complex products,” Chidambaram said in a public speech on Monday, reported by PTI. “If you want to sell insurance to India, you must sell simple products and must make it absolutely clear to agents and other officers that they should not mis-sell.”

Policyholders in urban India, where few buyers of insurance can claim they don’t have a rip-off story to tell, would know exactly what Chidambaram meant.

It’s a phenomenon that goes back to the first decade of privatization, when an around three-million-strong sales force, which took home up to 40% of the first-year premium as commission, sold life insurance products that were built like investor traps.

Complicit in this were life insurance companies that stood to benefit because of very high surrender charges (charges levied by the insurers when an investor stops paying premiums midway), as investors let policies lapse when they discovered that the policies were unsuitable.

According to a Goldman Sachs report, profits from the lapsed policies were enough not only to wipe out losses in some companies, but actually show profits at the aggregate.

The other group to benefit was the sellers of these products—agency commissions for the period 2004-05 to 2011-12 totalled Rs.1.13 trillion.

The mis-selling of life insurance products in the decade after the 2000 privatization is a textbook case of poor regulation and mis-managing the transition from a state monopoly to free markets. So big became the public uproar over the predatory sales of life insurance products that the regulator, in July 2010, was forced to step in and change the rules around the product being mis-sold—the unit-linked insurance plan (Ulip). But the damage had been done. Ulips, almost single handedly, have caused a deep erosion of investors’ money and confidence in the markets.

vinay mohanty

SELL RIGHT

"The best ways to keep people coming back are:

be believable, credible, attractive, responsive and empathetic."

SELL RIGHT

We believe you create a future, characterized by high performance and fulfillment, by making a responsible commitment to think right, work right, sell right, study right, and live right.

Here are ten strategies for forming the habit of selling right.

. Give it your best. Do every selling job to a finish and accept nothing but your best every time. As a professional salesperson, you are paid for the quality of service you provide with what you know, for those you know.

. Look like a winner. If you look like a winner, it's much easier to be one. You'll look as if you represent a reliable company. You'll look as if you're accustomed to influencing people and closing sales.

. Enjoy every sales call. Before every sales call, ask yourself this question: How would I feel about making this call if I knew it was going to be a good sale?

. Pay attention. Learn as much as possible about your prospects -- their reputations and capacities, who they are buying from now and what they are receiving for their dollars. Decide to be a shrewd observer.

. Build relationships. All things being equal, or not equal, prospects tend to buy from salespeople they trust, respect and like the most.

. Sell ethically. What is your ethical base? Can you articulate it? Can you identify how it influences your personal and professional behavior? Ethical behavior is doing the right thing, because doing the right thing is the right thing to do.

. Manage sales resistance. Realize resistance doesn't mean denial or refusal. In selling, it means, "Give me a reason to buy!"

. Close sales confidently. The most important factor in closing sales is not the customer. It's not the product. It's not the price. It's not the terms. It's not the weather or business conditions. It's you - the individual behind the sale - the closer who is thinking right and who has mastered a closing strategy.

. Develop endorsements. No advertising is as trusted as the spontaneous testimony of delighted customers. Expect endorsements.

. Serve what you sell. Never forget a client. Never let a client forget you.

"GO ALL OUT - NO IN BETWEEN IN 2013!"

Good luck and good selling,

vinay mohanty

How NRIs can buy LIC Policies?

NRIs can buy LIC Life Insurance cover under Non-Medical (Special) scheme or Medical scheme, depending on their health, sum insured they are opting for and where (country) they are working -

What is a Non-Medical (Special) Scheme?

1- Applicable if insurance is obtained during visit to India or through Mail Order Business (when LIC Agents visits the country of residence of NRI for completing the necessary formalities)

2- Maximum age at entry would be 45 years

3- LIC Plans with high risk cover and term rider benefits would not be allowed.

4- The proposer should be employed in Government or reputed commercial firm or should be a professional such as Chartered Accountant, Doctor, Teacher, Lawyer, Accountant, Engineer, etc.

5- This scheme is applicable to those NRIs who are residing in Group VI, VII and VIII countries only. ( See Annexure-V for group details).

What is a Medical Scheme?

When proposer has to undergo medical tests (special medical tests) to buy LIC Policies. Blood, Sugar, Heart, S.Chol, ECG, Thread Mill etc required as per policy Amount and age.

Who is a Non-Resident Indian as per LIC?

As per LIC following persons will be treated as NRIs for taking Life Insurance Policy -

1- A non-resident Indian is a citizen of India temporarily residing in the country of his/her present residence and holding a valid passport issued by the Government of India.

2- NRI should not be a green card holder. He/She should not have applied for or planning to apply in the near future for acquiring citizenship of his /her present country of residence or any other country.

3- It is clarified that People of Indian Origin having foreign nationality and residing in foreign countries (PIO) are not considered as NRIs for the purpose of allowing insurance.

What Documents Required by NRIs to apply for LIC NRI Life Insurance?

1- Prescribed Proposal Form depending on the type of policy selected (Form No. 300 in majority of the cases).

2- NRI Questionnaire (Annexure-II).

3- Medical Report (not applicable if the proposal is under non-medical scheme).

4- Special Questionnaire (Annexure-III) (if proposal is under 'Mail Order Business' and if the agent does not visit the country of residence of proposer).

5- Special Medical Reports, if called for.

6- Attested Copy of Relevant Pages of Proposer's Passport.

7- Proof of Age and Income.

8- Initial Deposit equivalent to Instalment Premium under the proposed plan of insurance.

Things to Take Care

1- Minimum Sum Assured allowed would be Rs. 2 lakhs and maximum would depend on conditions of insurability. However, under mail order business, maximum sum assured would be limited to Rs. One Crore only.

2- Personal Financial Questionnaire (PFQ) and/or Proof of income in the form of income tax returns, copy of employment contract where emoluments are mentioned, Certificate from Chartered Accountant, etc. would be required if the sum assured is high or if the proposal is submitted through Mail Order Business.

3- All types of plans are allowed subject to the conditions that -

a- Critical Illness Benefit is not granted.

b- Term Rider Benefit would be restricted to certain limit of Sum assured

c- Sum Assured would be restricted in respect of term insurance plans.

4- Policies are issued in Indian Rupees only

Are LIC's premiums higher for NRIs as compared to resident Indians?

No. The premiums are the same for residents and non residents. However, if NRIs are living in countries where risks are higher, premiums maybe higher.

Are there any limits on the sum assured?

In case of LIC policies, if the NRI chooses to conduct his medical examination in the foreign country, the sum assured will be limited to Rs 1 crore. If the NRI has his medical examination done on a visit to India, then he can get a higher cover. But it depends on individual underwriting.

vinay mohanty

IRDA has Revised Norms for Traditional Life Insurance Products

The Insurance Regulatory and Development Authority (IRDA) has revised the minimum death benefit and minimum surrender value norms for traditional life insurance products. Traditional life insurance products now come with a mandatory higher minimum death benefit and surrender value.

What is changed?

1- Minimum Death Benefit

For customers below 45 years, the minimum sum assured should be higher by 10 times (as against the existing five times) the annual premium or 0.5 times the annual premium multiplied by the term of the policy or 105 per cent the premium paid as on the date of the policyholder’s death.

2- Minimum Guaranteed Surrender Value

There is also a minimum guaranteed surrender value of 50 per cent of the total premiums paid, if the policy is surrendered in the second or third year while the same would be 75 per cent for the fourth year, and goes progressively upward.

What happen to Existing Policies?

Life insurers have been given time to withdraw group and individual policies before March 31 and June 30 respectively and have to file for product approvals afresh in line with the new guidelines.

Last year in June'2012, the IRDA issued a draft guidelines on the proposed above changes in life insurance products.

vinay mohanty

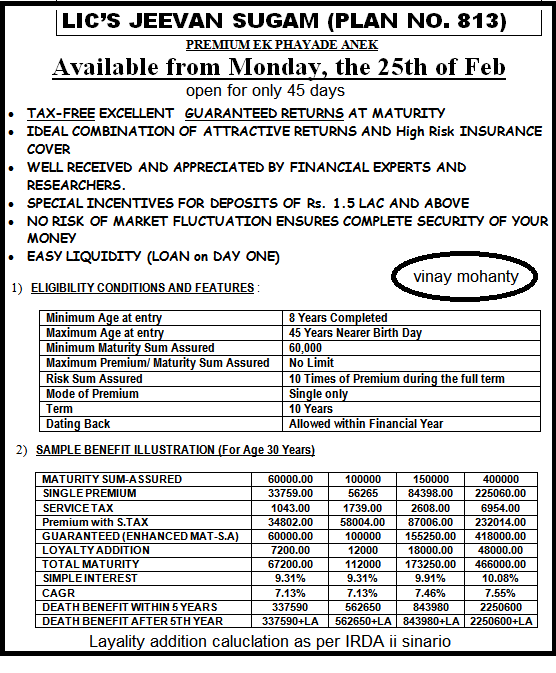

SUMASSURED ELIGIBILITY CONDITIONS

SUM ASSURED ELIGIBILITY CONDITIONS.

AGE Upto 30 years 22 times of gross Annual Income.

AGE 31 to 40 tears 17 times of gross annual income.

AGE 41 to 50 years 12 times of gross annual income

AGE 51 years and above 10 times of gross annual income.

vinay mohanty

LIC chairman on vision2020

click on billow link for chaiman merohotra,s statements

http://dl.dropbox.com/u/9243963/TOIM_2013_2_1_8.pdf

http://dl.dropbox.com/u/9243963/TOIM_2013_2_1_8.pdf

Subscribe to:

Posts (Atom)